Corporate tax rates are at the forefront of economic discussions as lawmakers prepare for a pivotal tax battle in 2025. With the expiration of key provisions from the 2017 Tax Cuts and Jobs Act looming, voters are more concerned than ever about how these changes will affect corporate tax revenue and the overall economic growth of the nation. Notably, political figures like Kamala Harris are advocating for higher corporate rates to finance various initiatives, while supporters of the Donald Trump tax cuts argue for reducing these rates further to energize business investments. A recent analysis highlights the ongoing debate regarding the effectiveness of past corporate tax changes and their real impact on wages and economic outcomes. As stakeholders weigh the benefits and pitfalls of different tax strategies, the conversation around corporate tax rates becomes increasingly critical for shaping the economic landscape ahead.

The discussion surrounding corporate taxation takes center stage as policymakers eyeball significant reforms in the coming years. As elements of the Tax Cuts and Jobs Act face expiration, crucial debates arise regarding the potential adjustments to corporate income rates. Advocates for increasing these rates, including some Democratic leaders, seek to enhance corporate tax revenue to facilitate new programs, contrasting sharply with the Republican stance favoring further reductions to stimulate economic activity. The ongoing scrutiny of corporate taxation continues to attract attention from economists and political figures alike, driving dialogues around equitable tax practices and their implications on economic prosperity. The future of the U.S. corporate tax landscape remains uncertain but vital for immediate and long-term financial strategies.

Understanding Corporate Tax Rates and Their Impact on the Economy

Corporate tax rates play a crucial role in shaping the economic landscape of a country. The reduction of the corporate tax rate from 35% to 21% under the 2017 Tax Cuts and Jobs Act (TCJA) was presented as a means to stimulate investment and economic growth. Proponents of this measure, including Donald Trump, argued that lower rates would incentivize businesses to invest more in their operations, leading to job creation and increased wages for workers. However, the empirical evidence has sparked a debate about whether these tax cuts actually delivered on their promises of significant economic boons or simply contributed to a decline in corporate tax revenue without substantial benefits to the overall economy.

In contrast, critiques from figures like Kamala Harris emphasize the need to raise corporate tax rates to fund essential social programs and correct budget deficits exacerbated by the TCJA. The report by Gabriel Chodorow-Reich and colleagues highlights a mismatch between the theoretical benefits of tax cuts and the actual economic outcomes observed in the years following the TCJA’s implementation. While there were modest increases in wages and capital investments, the overall decline in corporate tax revenue raises questions about the sustainability and long-term implications of such tax policies. It also brings to light the concept that reductions in tax rates do not necessarily correlate with a proportional increase in economic activity.

The Legacy of the Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act remains a defining piece of legislation in recent American economic policy. Enacted in 2017, this law marked a significant alteration to the corporate tax structure aimed at fostering economic growth. The act’s result was an immediate reduction in corporate tax revenue, which plummeted by 40% at the onset of the law’s implementation. Despite initial concerns about revenue loss, it later became evident that corporate tax revenues rebounded, largely due to higher-than-expected business profits. This rebound reflects a complex economic environment where businesses adapted to new global challenges, reshaping revenue streams in ways that some economic models failed to predict.

In analyzing the law’s impact, researchers like Chodorow-Reich have dissected the nuances of corporate tax cuts and their actual economic impact. While the TCJA aimed to encourage investment through immediate expensing provisions, the reality was a much more nuanced situation. For example, about an 11% increase in capital investment was noted following the cuts. However, many critics argue that this increase falls short when measured against the projected benefits. Furthermore, the expiration of certain provisions and the looming fiscal challenges ahead emphasize the need for a more balanced and strategic approach to tax reform—one that takes into account both the necessity for revenue generation and mechanisms to support long-term economic sustainability.

Debating the Future of Corporate Taxation

As the 2025 tax battle looms, the conversation around corporate tax rates has reignited discussions about fiscal policy, economic growth, and social responsibility. With key provisions of the Tax Cuts and Jobs Act set to expire, lawmakers are at a crossroads. Should corporate tax rates be raised to ensure adequate funding for public programs and reduce deficits, or should they be further cut to stimulate growth in a post-pandemic economy? The clash of perspectives typified by voices like Kamala Harris advocating for rate increases and Donald Trump favoring cuts illustrates the partisan divide that permeates this crucial issue.

The push for tax policy reform is compounded by ongoing economic challenges faced by the U.S. The COVID-19 pandemic reshaped how businesses operate and prompted unprecedented discussions about corporate accountability. The return of corporate tax revenue following the TCJA indicates resilience in some sectors but also raises questions about equity and fairness in taxation. As debates heat up, it becomes increasingly essential to understand how proposed tax changes will affect not just corporate balance sheets, but also job markets, wage growth, and overall economic equity in a country still grappling with the effects of wealth inequality and public investment needs.

Corporate Tax Revenue Trends Post-TCJA

Following the enactment of the Tax Cuts and Jobs Act, corporate tax revenue initially experienced a sharp decline, reflecting a significant 40% drop that worried fiscal analysts. However, the unexpected rebound in revenue in subsequent years has sparked further inquiries into its causes. Experts attribute this rebound not only to an increase in corporate profits—materially influenced by the unique circumstances of the COVID-19 pandemic—but also to strategic shifts in how companies reported their earnings in light of the 21% tax rate. This rise in profits highlights the complex interplay between tax policy and business operations in a globalized economy.

Yet, while corporate profits have soared, the implications for long-term stability and fiscal health remain under scrutiny. The performance of corporate tax revenue since the TCJA suggests a volatile relationship between tax cuts and actual economic contributions. Certain sectors, such as technology and pharmaceuticals, have thrived, contributing significantly to tax revenues. Still, this uneven distribution of economic benefits raises concerns about sustainability. As lawmakers consider the future tax landscape, the focus may need to shift towards ensuring that tax policies not only stimulate growth but also address the pressing funding needs for public programs and promote equity across different sectors of society.

Investments in Economic Growth and Corporate Tax Policy

One of the central arguments in favor of reducing corporate tax rates has been the belief that such cuts will lead to increased investment in the economy. Proponents of the Tax Cuts and Jobs Act posited that lowering the corporate tax burden would encourage businesses to reinvest profits back into their operations, leading to job creation and economic growth. Consequently, analyses, including those from Gabriel Chodorow-Reich and his co-authors, have highlighted that investments rose by approximately 11% after the implementation of these tax reforms, pointing to a correlation between lower tax rates and increased spending on capital.

However, the challenge lies in isolating the effects of tax policy from other influential factors affecting business investments. The pandemic altered many business dynamics, prompting companies to rethink their investment strategies. While the TCJA aimed to spur growth through tax incentives, it became evident that macroeconomic factors, such as supply chain shifts and consumer demand, also played pivotal roles in determining business investments. This realization has prompted economists and policymakers to rethink tax strategies, advocating for a more nuanced understanding of how different tax reforms interact with broader economic indicators.

The Political Landscape of Corporate Taxation

Corporate taxation remains a hotbed of political debate, particularly in the context of the upcoming 2025 tax discussions. As congressional leaders and candidates ramp up their proposals, the divide grows deeper between those advocating for increased corporate tax rates, such as Kamala Harris, and those pushing for further cuts, aligning with the views expressed by former President Donald Trump. The debates are not just academic; they touch on real-world implications for economic policy that affects millions of Americans, from workers to businesses and taxpayers.

The political ramifications of these discussions extend far beyond policy frameworks. They represent a broader ideological battle over fiscal responsibility, government spending, and social equity. With corporate tax revenues serving as an essential tool for funding public initiatives, finding common ground amidst starkly opposing viewpoints is crucial. As the expiration of key provisions from the TCJA approaches, the upcoming discussions will likely shape the future of corporate taxation in America, influencing economic growth trajectories and governmental fiscal strategies well into the next decade.

Lessons Learned from the TCJA Experience

The experience with the Tax Cuts and Jobs Act provides valuable lessons for future tax policy discussions. The TCJA illustrated that while cutting corporate tax rates can seem appealing for stimulating investment, the tangible benefits may not always align with the envisioned outcomes. While some sectors did experience growth, overall revenue trends indicated that cuts could contribute to significant budget deficits if not paired with robust measures to ensure adequate revenue streams. Furthermore, the notion that tax cuts automatically lead to increased corporate investment has been called into question by empirical data.

A critical takeaway from the TCJA experience is the importance of accompanying tax cuts with provisions that promote long-term investments and fiscal responsibility. Experts, including Chodorow-Reich, suggest that lawmakers should consider strategies such as reinstating overhauled expensing allowances while balancing these incentives with reasonable corporate tax rates. By learning from the nuanced outcomes of the TCJA, policymakers can pioneer tax frameworks that not only foster economic growth but also address pressing societal needs, ensuring a more equitable distribution of economic benefits.

Corporate Taxation in a Globalized Economy

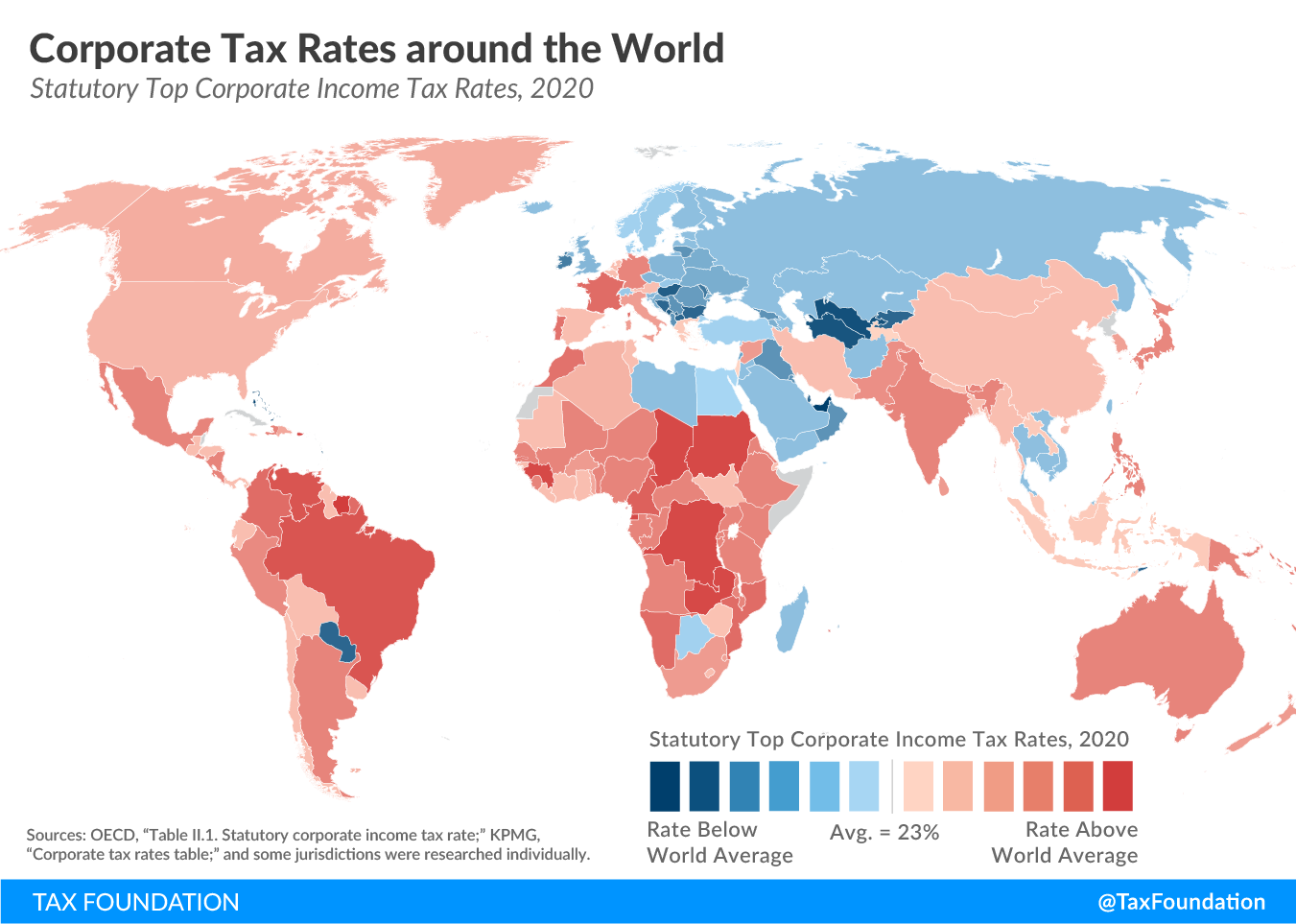

In an increasingly interconnected global economy, the implications of corporate tax policy extend well beyond national borders. The competitive nature of global markets has prompted many countries to reassess their corporate tax structures, often leading to substantial reductions in rates to attract foreign investment. As highlighted by Chodorow-Reich, the U.S. corporate tax rate was once positioned competitively compared to peers. However, by 2016, it sat at the higher end, compelling many U.S. companies to reconsider their international tax strategies and operations to remain competitive.

The ramifications of international tax competition significantly influence domestic policy discussions regarding corporate tax rates. As countries like Ireland make headlines for their low tax rates, many U.S. multinationals find themselves adapting to maintain profitability. This pressure amplifies the call for reforms to the corporate tax structure to ensure U.S. companies aren’t hindered by a burdensome tax environment. Therefore, navigating these complex global dynamics is essential for creating a corporate tax framework that balances the need for competitiveness with government revenue requirements.

Frequently Asked Questions

How did the Tax Cuts and Jobs Act affect corporate tax rates in the U.S.?

The Tax Cuts and Jobs Act (TCJA) of 2017 permanently reduced the corporate tax rate from 35% to 21%. This significant change aimed to make U.S. corporate tax rates more competitive globally and was expected to reduce federal corporate tax revenue by $100 to $150 billion annually over a decade.

What are the implications of raising corporate tax rates as suggested by Kamala Harris?

Kamala Harris proposes raising corporate tax rates to fund initiatives benefiting low- and middle-income households. Higher corporate tax rates could potentially increase government revenue, but the impact on business investment and economic growth remains debated among economists.

Did the Donald Trump tax cuts lead to increased corporate tax revenue?

Initially, the Trump tax cuts under the TCJA resulted in a 40% decline in corporate tax revenue. However, from 2020 onwards, corporate tax revenue rebounded significantly as business profits surged, surpassing earlier predictions. This phenomenon suggests that some businesses thrived post-tax cuts despite the initial revenue drop.

What effect did the TCJA have on economic growth and corporate investment?

According to studies co-authored by Harvard economist Gabriel Chodorow-Reich, the TCJA contributed to an 11% increase in corporate capital investments. However, while the tax cuts stimulated some investment, the overall growth in wages attributed to these tax cuts was modest, closer to $750 per employee annually.

What are the popular measures in the TCJA that influenced corporate policy?

Key provisions of the TCJA allowed for immediate expensing of capital investments, which were more effective in driving corporate investments than general tax rate reductions. These measures aimed at encouraging businesses to invest in growth and innovation.

How do corporate tax rates compare internationally after the Tax Cuts and Jobs Act?

Before the TCJA, the U.S. corporate tax rate was among the highest in the developed world. After the TCJA reduced the rate, the U.S. became more competitive, as many other countries had been lowering their corporate tax rates, making the global tax landscape more favorable for U.S. businesses.

What evidence exists regarding the impact of corporate tax cuts on wages?

While proponents of the TCJA asserted that tax cuts would lead to significant wage increases (estimated at $4,000 to $9,000 per employee), studies indicate that actual wage growth attributable to these cuts was around $750 per year, highlighting a disparity between expectations and outcomes in wage growth.

Will key provisions of the TCJA expire, and what could that mean for corporate tax rates?

Yes, many key provisions of the TCJA are set to expire by the end of 2025, including significant cuts to corporate tax rates. As Congress debates future tax policy, there may be a push to reinstate some expired provisions or raise corporate tax rates again to address budgetary concerns.

What role do expiring provisions in the TCJA play in discussions about corporate tax rates?

The expiration of provisions providing immediate expensing for investments has become a focal point in discussions about corporate tax rates. Experts, including Gabriel Chodorow-Reich, suggest that lawmakers might consider raising corporate tax rates while reinstating these expensing provisions to balance revenue needs with investments.

| Key Points | Details |

|---|---|

| Corporate Tax Rates Discussion | Debate on raising or cutting corporate tax rates amidst upcoming elections. |

| Impact of the TCJA | The 2017 Tax Cuts and Jobs Act reduced corporate tax rates from 35% to 21%, resulting in significant revenue loss. |

| Wage and Investment Effects | Wages increased modestly, while business investments saw an 11% rise under certain provisions. |

| Bipartisan Agreement on Reform | There was broad acknowledgment that reform was necessary due to the outdated corporate tax code. |

| Recommendations for Future Tax Policy | Consider restoring expensing provisions while potentially raising statutory rates to generate revenue. |

| Current Trends in Corporate Tax Revenue | After an initial decline, corporate tax revenues experienced a rebound post-2020 as firms reported greater profits. |

Summary

Corporate tax rates are once again at the forefront of political debate as new analyses reveal their impact on the economy. The 2017 Tax Cuts and Jobs Act has set the stage for a critical discussion in 2025, focusing on whether to raise, cut, or adjust these rates as various provisions approach expiration. The insights from recent studies highlight the complexity of corporate tax policy and its effects on investment, wages, and overall tax revenue, suggesting that prudent adjustments may lead to beneficial economic outcomes.