The commercial real estate crisis is looming over the U.S. economy as soaring office vacancy rates threaten to destabilize financial markets. With businesses embracing remote work, demand for office space has plummeted, creating vacancy rates between 12% and 23% in major cities like Boston. This uptick in empty buildings not only drives down property values but also raises alarm over an impending wave of real estate loans that are set to come due in 2025, potentially leading to bank failures. As interest rates remain stubbornly high, financial experts warn that delinquent loans could trigger significant repercussions across the banking system. The interplay between commercial property markets and broader economic health adds urgency to discussions about the future of corporate real estate in America and its far-reaching effects on the financial landscape.

As we explore the current difficulties in the commercial property market, it becomes evident that challenges persist in the realm of business real estate. The ongoing office building crisis signals a troubling trend, exacerbated by diminished demand brought about during and after the pandemic. Elevated office vacancy levels have led to concerns surrounding the stability of real estate holdings and the impending maturity of countless property loans in the near future. Moreover, the cumulative effect of rising interest rates makes it increasingly difficult for investors to navigate this volatile landscape. Observations regarding regional bank vulnerabilities and potential knock-on effects on the broader economy underscore the importance of addressing these real estate challenges promptly.

Understanding the Current Commercial Real Estate Crisis

The commercial real estate crisis in the U.S. is underscored by escalating office vacancy rates in major cities, which currently range from 12 to 23 percent. This surge in empty office spaces can be traced back to the pandemic, which has significantly altered the working habits of many businesses. With the prevalence of remote and hybrid work models, the demand for traditional office buildings has drastically declined. Consequently, the value of commercial properties has been adversely affected, and experts are raising concerns about the potential impact of this crisis on the overall economy.

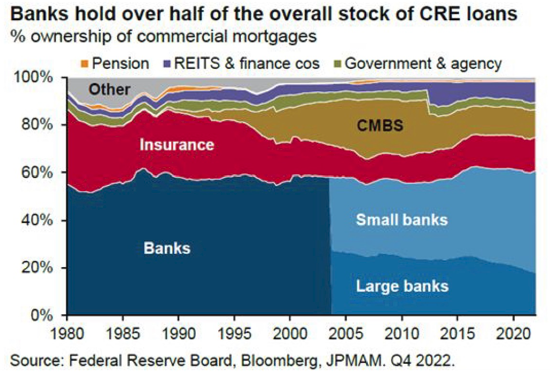

As the Federal Reserve maintains high interest rates in response to inflationary pressures, many property owners are facing a daunting wave of mortgage repayments. By 2025, approximately 20 percent of the $4.7 trillion in commercial mortgage debt held by lenders will come due. This scenario raises the stakes for regional banks and financial institutions that have vested interests in commercial real estate. If a significant number of these loans become delinquent due to failing property values, banks could face severe financial repercussions that may echo throughout the U.S. economy.

The Relationship Between Bank Failures and Real Estate Loans

With a substantial portion of banks’ assets tied up in real estate loans, the potential for widespread bank failures is a noteworthy concern as the commercial real estate crisis unfolds. Kenneth Rogoff, a prominent economist, suggests that while smaller banks may experience significant losses, the larger banking institutions, which have faced stricter regulations since the 2008 financial crisis, are more likely to withstand the storm. Yet, the ripple effect of failing regional banks might still destabilize local economies, leading to stricter lending conditions and decreased consumer spending.

Though major banks like Bank of America, Citi, and JPMorgan are better positioned to absorb shocks due to their diversified portfolios, the looming crisis in commercial real estate cannot be ignored. A sharp rise in bankruptcy declarations within the real estate sector could compel these banks to reassess their exposure to risky loans, potentially leading to lending tightening that could further stall economic growth. The situation is precarious, with the fate of many regional banks hanging on the health of their commercial real estate investments.

Exploring the Impact of Office Vacancy Rates on the Economy and Real Estate Market—

How High Office Vacancy Rates Affect Local Economies

High office vacancy rates pose significant challenges that extend beyond the immediate real estate market. When office buildings remain unoccupied, property values drop, adversely affecting local tax revenues that municipalities rely on for public services. This can create a negative feedback loop where local governments are forced to cut budgets, leading to reduced public services and infrastructure improvements. Furthermore, with fewer businesses operating in these spaces, there is a reduction in economic activity, impacting local shops, restaurants, and service providers who depend on office workers for patronage.

In addition to governmental impacts, high vacancy rates can strain regional banks that hold commercial real estate loans. If property owners cannot lease their spaces and fail to meet mortgage obligations, banks may face stiff challenges that could lead to loan defaults. Over time, this could destabilize the local banking environment, leading to tighter credit conditions that would further inhibit economic recovery and reduce consumer spending. Consequently, addressing the current high office vacancy rates is crucial not only for the health of the commercial real estate sector but the broader economy as well.

The Role of Interest Rates in the Commercial Real Estate Crisis

Interest rates significantly influence the commercial real estate market dynamics. Prior to the pandemic, low interest rates facilitated robust borrowing and investment in commercial properties, leading to a surge in funding for numerous ventures. However, as the Federal Reserve has now adopted a more hawkish stance by maintaining elevated interest rates in an effort to combat inflation, property investors are faced with increased borrowing costs. This has put pressure on developers and property owners, resulting in difficulties in managing existing debts as the value of their real estate holdings declines.

The rise in interest rates also exacerbates the risks related to refinancing existing loans that are maturing. Many commercial properties that were financed during more favorable conditions are now at risk of defaulting as interest expenses rise. This environment of heightened borrowing costs affects not only the real estate market but also has broader repercussions for the U.S. economy. As properties lose value and occupancy rates remain low, financial institutions must brace for potential floodgates of delinquencies, which could significantly impact their financial health and lending capabilities.

Potential Reforms to Mitigate the Crisis in Commercial Real Estate

As the commercial real estate crisis unfolds, experts are advocating for several reforms aimed at alleviating the burden on both property owners and financial institutions. For instance, adjustments in zoning laws could facilitate the conversion of underoccupied office buildings into residential spaces, providing alternative uses for these properties. This shift could help stabilize property values and generate income, albeit with considerations on structural adaptations that may be necessary for such transitions.

Additionally, reforming how banks manage their exposure to commercial real estate loans may be necessary. Implementing stricter capital reserve requirements for smaller banks that are heavily invested in real estate could shield the banking sector from the repercussions of a downturn. Furthermore, offering incentives for lenders to restructure loans or providing temporary relief measures could enhance the situation for borrowers facing financial difficulties. These reforms could foster resilience in both the real estate and banking sectors, ultimately stabilizing local economies.

Analyzing the Long-term Outlook for Commercial Real Estate

The outlook for commercial real estate remains complex as high vacancy rates and rising interest rates continue to pose significant challenges. While certain segments of the market may show resilience, such as properties with premium amenities, the overall landscape is fraught with uncertainty. The anticipated increase in delinquent loans among regional banks poses a risk that could significantly impact their financial standing, leading to tighter credit and reduced investment in local economies.

Moreover, analysts suggest that while conventional wisdom expects a recovery by 2025 with lower interest rates, structural challenges within the sector might prolong this crisis. Investors currently adopting a ‘stay alive till ’25’ mentality may encounter disappointment if economic conditions do not improve as anticipated. Thus, stakeholders must remain vigilant, adapting strategies to navigate the evolving challenges of commercial real estate while preparing for the possibility of continuing fluctuations in the economic landscape.

Frequently Asked Questions

How do bank failures relate to the commercial real estate crisis?

Bank failures can be closely tied to the commercial real estate crisis because many banks have significant exposure to real estate loans. When commercial properties, particularly office buildings, experience high vacancy rates and declining values, this can lead to increased delinquencies on loans. As banks face rising losses, particularly among regional banks that are more heavily invested in commercial real estate, the risk of failure escalates, threatening the broader financial system.

What are the consequences of high office vacancy rates on the U.S. economy?

High office vacancy rates are a significant concern for the U.S. economy as they lead to decreased property values and impact banks holding commercial real estate loans. This situation can cause financial strain on regional banks, potentially leading to tighter lending conditions which hampers economic growth. Furthermore, as banks suffer losses, this can spill over into other sectors, affecting consumer confidence and spending.

How do interest rates influence the commercial real estate crisis?

Interest rates play a crucial role in the commercial real estate crisis as rising rates increase the cost of borrowing, making it harder for investors to refinance existing loans. This situation can lead to higher vacancy rates as more businesses downsize or close, influencing property values negatively. The Federal Reserve’s reluctance to lower interest rates further complicates the recovery, increasing the pressure on already-struggling commercial properties.

What impact do real estate loans have on the financial stability of banks?

Real estate loans are pivotal to financial stability for banks, particularly at a time when a wave of commercial real estate loans are coming due. If borrowers fail to repay these loans due to declining property values and high vacancy rates, banks may face substantial losses. This exposure is particularly acute in smaller regional banks that may not have the same level of regulatory capital buffers as larger institutions, increasing the risk of bank failures.

Can the commercial real estate crisis lead to a broader economic downturn?

While the commercial real estate crisis poses risks, it is unlikely to trigger a full-blown economic downturn unless coupled with a severe recession. The broader U.S. economy shows resilience with a robust job market and a thriving stock market, although losses in commercial real estate could hurt regional banks and consequently, local economies. The interconnectedness of financial institutions means that significant distress could lead to tighter credit availability, potentially impacting economic growth.

How might banks respond to looming delinquencies in commercial real estate loans?

To mitigate the risks posed by looming delinquencies in commercial real estate loans, banks may tighten lending standards, reducing the availability of credit. Additionally, they may increase provisions for bad debts to account for potential losses, affecting their profitability. Larger banks are likely to be better positioned due to stricter regulations and diversification, while smaller banks may struggle and could face forced consolidations or failures.

What is the outlook for the commercial real estate market amid rising interest rates?

The outlook for the commercial real estate market remains challenging amid rising interest rates. With increased borrowing costs, potential for high office vacancy rates, and a significant surge of loans maturing by 2025, the market may continue facing downward pressure. Investors are hopeful for a decline in long-term interest rates, which could alleviate some financial burdens, but currently, many properties are over-leveraged and struggling to maintain occupancy, complicating recovery prospects.

What are the long-term implications of the commercial real estate crisis for investors?

Long-term implications of the commercial real estate crisis for investors include potential significant losses as property values decline and occupancy remains low. Investors in real estate funds, including pension funds, may need to adjust expectations for returns. The transition period could result in bankruptcies and restructuring within the sector, but some investors might benefit if they hold onto quality assets during market corrections and the eventual recovery.

| Key Point | Details |

|---|---|

| High Office Vacancy Rates | Vacancy rates in major U.S. cities range from 12% to 23%, impacting property values. |

| Commercial Real Estate Debt | 20% of $4.7 trillion in commercial mortgage debt is due this year, raising concerns. |

| Risk of Bank Failures | Less regulated small and medium-sized banks face greater risks of failure due to real estate losses. |

| Investor Optimism | Investors hope lower long-term interest rates will resuscitate the real estate market. |

| Consumer Impact | Potential losses to pension funds and local economies, yet robust job and stock markets mitigate broader damage. |

| Large Banks’ Resilience | Larger banks are better prepared due to diversification and profitability in other areas. |

Summary

The current commercial real estate crisis poses significant challenges for both investors and regional banks. As vacancy rates soar and a high volume of loans comes due, the risks of bank failures appear heightened, particularly for smaller institutions. Nevertheless, the broader U.S. economy remains resilient, supported by a strong job market and active stock investments. The path forward hinges on interest rate adjustments and how well banks and investors navigate this impending wave of challenges.